One Broke Mum: 'The terrifying moment I realised I wouldn't have enough money to retire'

By Jo Abi|

It's a terrifying moment to realise you don't have enough money for retirement. Actually, come to think of it, it's terrifying to be of an age that you begin to think realistically about what retirement will be like!

I turn 44 in January, and due to a series of serious financial setbacks, retirement is going to be difficult, if not impossible.

That's after being employed since I was old enough to get a proper job at the age of 16, so to say I am disappointed is an understatement.

To say I am worried is an understatement.

I am a single mother of three children - Philip, 15, Giovanni, 11, and Caterina, 10 - so there isn't much money to go around. I'm flat out paying the bills without putting extra money away in superannuation.

I also don't own any property, nor do I have any savings to speak of, unless you count the $60 I am holding onto between now and pay day.

Look, it is what it is, and I refuse to panic. Well, I did panic, but then I started doing some research, and there are a few things I can do to ensure my twilight years are the best they can be.

There are simple ways we can all increase our super and the sooner you start, the better your retirement will be.

**Please consult your superannuation fund or financial adviser before making changes to your superannuation and retirement plans.**

Easy ways to increase your super

1. Find all of your super

By the time you reach an age at which you begin to worry about your super, you've probably had several jobs, which can often mean a trail of superannuation accounts in your name.

Thankfully, it's easy to find them all using the website LostSuper.com.au. You just need your tax file number.

The hard part is rolling it all over into the superannuation account of your choice which is fiddly and involves a lot of paperwork.

Set aside your next life admin day and get it done. It's well worth it.

2. Ensure you are with an industry super fund

Industry super funds are not-for-profit, which means they charge lower fees when compared to retail super funds, and all profits to back to members. I have been told this is the best choice, and am happy with my super fun.

You can find out more about the best super fund for you, whether it be an industry or retail fund, by visiting Canstar.com.au.

Compare their returns and choose the one with the highest to maximise your superannuation.

3. Make voluntary contributions

My accountant (my sister Marina) has been hassling me to make voluntary contributions to my superannuation for years.

"It's tax deductible Jo! Just get your employer to do it for you!!!!"

I asked her to tell me more and she said anyone can pay between $25,000 and $100,000 a year into their superannuation accounts while benefiting from tax offsets and deductions.

You can find more details on this on the ASIC website.

As one of the many (majority) of Australians who doesn't have that sort of money, I'm thinking of making smaller contributions on a regular basis.

Marina said it doesn't matter if I ask my employer to make extra super contributions on my behalf with before-tax-dollars or if I do it myself via direct debit with after-tax-dollars, because any contributions I make are tax deductible.

"Ask work to put extra money into super from your pay so it reduces your personal tax," she suggested. "Or you can just set up a direct debit from your account. It's the same tax wise. Any extra super you pay is a tax deduction."

I'm going to start with $50-$100 a month, which will be a stretch, but if I work for another 20 years that's an extra $12,000-$24,000 in my super account.

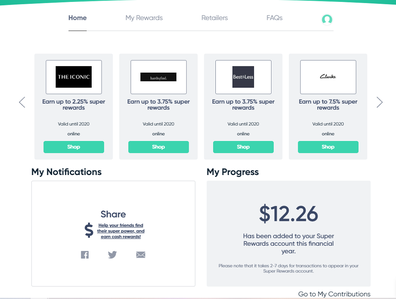

4. Use Super Rewards for all your shopping

While researching this article, I received a PR email about a new Australian website called Super Rewards. Apparently by doing all my online shopping using Super Rewards, they pay money back into my super for every purchase.

**Don't accidentally go to the Super Rewards company in the US. The one I am discussing is super-rewards.com.au, an Australian-based platform.**

I spoke with co-founder and CEO Pascale Helyar-Moray, and she said she and her partner were motivated to start the service because they were concerned about the pay and therefore superannuation disparity that still exists for Australian women.

"You go to the platform and you choose Woolworths, you do your shopping on the Woolies site and Super Rewards tracks the spend," she explains. "They will then pay 1.75% of the value of the grocery shop into your super.

"So if you spend $300, you earn $5."

It sounds genius to me.

Super Rewards just went live and setting up my account was easy. I just needed all of my personal details, my superannuation account details and my tax file number.

I made my first purchase using Super Rewards at the weekend when I bought an affordable dining set for $590 at Catch.com.au and I can't wait to track my first super contribution!

But a word to the wise - this isn't an excuse to do extra shopping online. Stick to your budget and your usually spending behaviours. Just do what you can through Super Rewards.

Retails on the site include Woolworths, Catch.com.au, Booktopia and so many more.

5. Don't release your super early for any reason

During the Global Financial Crisis (GFC) in 2008/2009 my then husband's business went bust, and so I released $50,000 of my superannuation to catch up on our insane debts. He did the same.

Majority of the money released went to mortgage payments on our home. I remember reading at the time that statistically, something like 90% of people who release super to catch up on mortgage payments lose their homes anyway.

I thought we'd be different. We weren't. We lost our home anyway and with it, $50,000 that would have been for my retirement.

Try and avoid releasing your super if at all possible, aside from reasons out of your control such as emergency medical treatments. In my opinion, that's the only reason to dip into your retirement savings.

Everything else can ideally be managed through insurance companies and your loan providers. What I found, as we were going under, was that businesses we owed money to just wanted us to stay in contact with our plans to catch up on our debts, and even the most minor of payments was considered as an intention to pay, so they were more reasonable when it came to waiving late fees.

You can contact Jo Abi at jabi@nine.com.au or via Instagram @joabi_9 or on Twitter @joabi.